The SEC has decided that short selling has gotten out of hand. The practice in which shares are borrowed and sold, hoping to be bought again at a lower price and returned in order to generate profits when a stock is falling, is a common practice among investors who feel a stock is overpriced. Financial stocks have been shorted heavily in the past year, Bear Sterns Cos (BSC) being case in point. When it was rumored to be in trouble, millions of shares were shorted, aiding the downfall of the company.

Today the SEC moved to curb excessive short selling by eliminating 'naked shorting' in which shares aren't actually borrowed. The idea is that as long as the institution could obtain shares it can allow shorting, it doesn't actually have to go through with the process of finding them. Starting Monday the practice will no longer be considered legitimate. Financial stocks which have bear ed the brunt of the short sellers rose hugely today, as investors bet the prices will start to rise once naked shorting is ended. Examples include Lehman Bros (LEH) which has risen over 50% since Tuesday, and Citigroup (C) which rose over 18%. Also seeing some day light are government backed Fannie Mae (FNM) and Freddie Mac (FRE) which are up 12.33% and 17.16% respectively.

This ruling is in a way a double edged sword for financial stocks. In the short term, it provides much needed relief from the battering their stocks were taking from short sellers. Also, it gives confidence to investors that the government will not stand for speculation to get in the way of the macro economy functioning. This can be seen from the recent price jumps. However, in the longer term, it may end up keeping profits down in the future. Many of these companies profit from not only arranging naked shorting, but do it themselves. The elimination of the practice, and continuing regulation by the government could cut into the incomes of these financial stocks in the future.

I am overjoyed that the market actually had a couple successful days among the weeks of crap we have seen, but I do find it interesting that this may come back to haunt the same institutions that are reaping the benefit currently. I'm hoping that the bulls can find their legs again, at least among deserving companies. I think that they may have gotten a little closer these past couple days.

Thursday, July 17, 2008

Sunday, July 6, 2008

Why I think the Housing Bubble is Barely Burst

So I did a research project/paper this past winter/spring about US homes prices, whether or not prices were a bubble and what was going to happen if indeed the market was inflated. I concluded that yes there was a bubble, it had already started to collapse and it would probably continue for a while because prices seemed to have rose way too rapidly over the past decade.

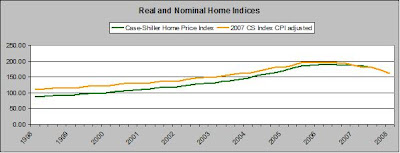

What I didn't realize was how inflated home prices were. A little background info is needed before I start. Dr. Robert Shiller, a professor at Yale and foremost economist when it comes to home prices, wrote a book called Irrational Exuberance in 2000 in which he predicted the tech bubble burst. Then in 2005, he re-released the book with new content that essentially called out the housing bubble burst. He shows in the book through a exhaustive index he created charting home prices that on average, prices rise about .4% a year, when inflation is factored in. From 1940 to 2000, prices rose an average of .7% a year. You get the idea that homes are not great investments from a pure, return-oriented view.

So, how much did homes increase in real value from 1987-1997? None. Actually less than none: -8.46%. The next decade? Home prices increased in real value 82.55% from '88 to their peak in real value in late 2005. Nominal (or not adjusted for inflation) values peaked in 2nd Quarter 2006. Comparing the two decades shows a sharp contrast.

What makes me believe that home prices still have a ways to fall is not simply how inflated prices were, but why they were so inflated. Home prices were so inflated because of increased demand for homes, fueled by a huge increase in credit availability. Basically, when more people can buy homes, demand increases and prices do too. It's not hard to see that right now credit is being restricted and new loans are subject to scrutinization as apposed to securitization. Home prices were a large, juicy bubble, growing ever bigger by lenders, real estate agents and consumers who all believed they could ride the bubble endlessly. They were wrong. All bubbles eventually pop. Whether it be the Stock Market Crash or the tech bubble, when prices are growing only because people expect them to continue to climb, there is a bubble present. Watching home prices tumble and comparing them to technology stocks' plummet in 2000 is easy to do, and probably a reasonable jump to make. While homes have greater intrinsic value than domain names with 25 million in short term debt with no revenue stream did in 2000, they both grew in price because of irrational exuberance, and were brought down by rational investors who figured the bubble out.

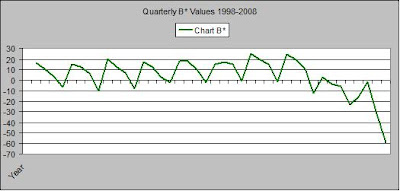

I did some analysis of the data i collected from my paper, updated it, and tried to get an idea of how far prices need to fall in order to be back down to a 'fair' level. What I found shocked me. I'm not going to pretend for a second that I am some sort of math wizzzzard who can predict all markets, but this model did predict prices to fall by a ton, which they have been doing. Basically, I derived a variable, Beta, that is an indicator of how overprices or under priced a asset is. A Beta of 1 means perfectly priced, under 1 ins undervalued and vice versa. Below is the Beta values by quarter over the past decade.

I integrated the curve charting quarterly Beta values and found the displacement from where they should be (equilibrium.) Then I looked at how much they have been displaced so far since the bubble 'burst.' I took A-B=C. C being the amount left to burst. Then I used that number to find out how much prices would fall. The number? 41.209% Shhhhhit.

Do I think home prices will fall 41.209% No. Close to that? Probably not. This number was generated using the assumption of .7% real increase a year being the expected return of a home, and I think that that number is dated. It does show, however, how far prices could fall if long run historical norms are still relevant. I suspect that if prices fall another 20%-25%, buyers will flood the market and prices will begin to return to normal. However, I expect prices to fall at least another 15%-20%, and home prices will probably not return until normal for at least 2 or 3 years.

What does all this mean? It means don't make any investments planning on homes prices rebounding any time soon. Default rates will stay dismal as long as home prices are low, which means more write downs for banks. We're seeing this already, and I think it may continue in a slow and painful way for a while. It doesn't mean I think the stock market will be poor for another 3 years, or even that financial stocks will. But companies that have direct exposure to home prices may be hurting for the short term. Take this with a grain of salt. Do your own research, and let me know what you think. If you would like a more detailed explanation of the model I'm using, or have questions/comments/criticisms, hit me up. (drewo88@hotmail.com)

Friday, July 4, 2008

What To Do Now

While watching the market tank everyday-many days opening high and then crashing after a couple of hours-has me down. As I said before, I thought that the worst was behind us, and I was wrong. Since I started sharing my long term picks on this site (see lower left) The S&P 500 is down more than 5%, but the worst part is that the market had jumped over 7% before losing it all and then some. This makes me sad because I feel like a optimistic dumb-ass. I lost about 15% on holding Citigroup (C) long, and finally closed out a little while ago, feeling that I might as well cut some losses. I also closed out the long position on Vale ADR (RIO), as I felt bears were swamping almost all stocks, and I'd like to preserve some gains.

However, I did add one long position to my portfolio: Wal-Mart (WMT.) As I have talked about before (See My recession article ) I think WMT is a great play when the economy is doing ugly things. While low consumer sentiment, high unemployment and even higher gas prices may seem like big negatives for a retailer, WMT is different. Wal-Mart provides really cheap, yet quality goods, which is good for people who feel the economy is doing poorly and don't have jobs but still need food and toilet paper. Also, WMT has pretty much everything you could need at one location, and so for those who don't feel like driving around on $5 gas it serves as a one stop shop. All of these bode well for WMT. They keep costs low, drive away competition because of it and when people are short on cash, look incredibly attractive when it comes to buying the necessities. They also look good to me as a company that can survive these dire times.

However, I did add one long position to my portfolio: Wal-Mart (WMT.) As I have talked about before (See My recession article ) I think WMT is a great play when the economy is doing ugly things. While low consumer sentiment, high unemployment and even higher gas prices may seem like big negatives for a retailer, WMT is different. Wal-Mart provides really cheap, yet quality goods, which is good for people who feel the economy is doing poorly and don't have jobs but still need food and toilet paper. Also, WMT has pretty much everything you could need at one location, and so for those who don't feel like driving around on $5 gas it serves as a one stop shop. All of these bode well for WMT. They keep costs low, drive away competition because of it and when people are short on cash, look incredibly attractive when it comes to buying the necessities. They also look good to me as a company that can survive these dire times.

Subscribe to:

Posts (Atom)