I haven't written an article in a matter of months, and to those who still check this blog I apologize. It is not that I do not want to write, but just that I didn't feel I had much to say that was constructive or useful. I, as most, have been at a loss over the past months as stocks have plummeted and the financial crisis has worsened. While I still have little insight into the equity market, I do feel that there is a situation developing within the oil market.

One of the few things I was sure about 6 months ago was that commodities, especially oil and gold, were in a bubble brought on by inflation worries and a rush of investor money fleeing the stock market.We have watched oil prices move from highs around $150 per barrel to a current spot on the NYMEX of crude oil at $39.82. That's more than a 73% decrease in price, in just a few months. Gas prices went from an average over $4 per gallon to a national average well under $2. No one is talking about oil anymore, unless they are commenting on its epic slide.

I think that oil is a BUY. Oil, while once over-valued, has gone below what most were calling fair value (between $60-80 a barrel) and has continued to fall, even with talks of an OPEC intervention. While I knew that oil's very short term demand was more elastic than many guessed, as we can see by the fall in oil's price, its longer short term demand is not so. It will take years for us to get off oil, and we are no where close currently. This huge decrease in price is going to stop advancement of alternative energy for a while. Prices will begin to rise again, and there is nothing stopping oil returning to previous levels. With OPEC slashing supply, prices will eventually rise. Even if oil only returns to fair value, it represents a $20 per barrel increase. This is a more than 50%. While I bet against oil and gold when the commodities were over-priced, I will now bet with oil because it is undervalued. Unlike stocks, oil does not have mortgage debt exposure. It has intrinsic value, and there seems to be little long term downside, as oil will be in demand for at least another 20 years.

I see a possibility that oil could drop to lower levels, possibly even below $30. However, I doubt this, and I think there is a much greater chance that oil prices rise. This is why I think oil is a buy right now, because I believe oil is nearing its trough.

Ways to Invest Without Writing Futures Contracts

The best way to gain exposure to oil, in my opinion, is through an ETF. Though there are some fees, it greatly reduces complications of writing contracts, and is relatively liquid (especially the ones I choseto highlight). The best ones I've researched:

Ticker: OIL (NYSE)

Full Name: Goldman Sacs Crude Oil Total Return ETN

YTD High/Low Price (% change): 86.90/21.68 (-75%)

More Info

Ticker: DXO

Full Name: PowerShares DB Crude Oil Double Long ETN

YTD High/Low (% change): 28.78/2.30 (-92%)

More Info

Ticker: DBO

Full Name: Powershares DB Oil Fund ETF

YTD High/Low (% change): 54.93/18.22 (-66.83%)

More Info

Let me know what you think.

Monday, December 22, 2008

Monday, September 8, 2008

Will the Governments Move Work?

Over the weekend the US Government, led by the Federal Reserve, The Treasury Department and Federal Finance Housing Agency, took over Fannie Mae (FNM) and Freddie Mac (FRE) in a move that shows unprecedented central mingling within the world of finance. Fannie Mae and Freddie Mac, which were already semi-public institutions were essentially forced into the deal which gives control to the US Government through preferred stock. In turn the gove rnment will prop up the mortgage lenders who's books are swamped with debt.

rnment will prop up the mortgage lenders who's books are swamped with debt.

FNM and FRE are down close to 90% today, as they both are trading under a dollar a share. Henry Paulson, Treasury Secretary Henry Paulson stressed that the bailout was to prevent a massive, potentially worldwide financial melt-down, not to bail out investors who had made a poor bet on the companies, or who believed that the fact FNM and FRE are government backed meant their investments were without risk.

The question is now whether this move is enough to turn the markets around, speed stocks to recovery and move our economy toward productive growth. Though stocks surged today, up almost 3% today, there still remains great uncertainty whether this move will actually solve the problems we face today.

What do I think? Honestly, while I think the move is a needed one to prevent a much larger problem, I do not believe that our economy will be magically cured over night by the move. Home prices are continuing to fall, and until they trough and begin to recover, defaults will rise, write-downs will mount and the overall economy will be shaky. I do, however, think that this could be the bottom for some stocks, if not the market in general. Last time the government made a large, unprecedented move to keep the markets afloat, after Bear Sterns, we enjoyed a few months of higher levels of trading before the bears came again. I think that we will definitely see stocks trading up, but they may actually stay high this time. The dollar is recovering, but it is still low enough to keep exports high, and commodities, especially oil, are trading down due to crack downs on speculation in these markets.

Overall, I think that this will be very interesting next few months. Hopefully stocks will recover, banks will start to find a foothold and buying opportunities will present themselves. The main indicator I will be watching is home prices and defaults. If you think you see a bottom in prices or a top in defaults, I'd say that's the time to jump in. I think home prices will continue to drop, however, though not as much as predicted in my last article because this move by the government will stabilize the housing market. I'm gonna watch closely and wait for this to happen.

rnment will prop up the mortgage lenders who's books are swamped with debt.

rnment will prop up the mortgage lenders who's books are swamped with debt.FNM and FRE are down close to 90% today, as they both are trading under a dollar a share. Henry Paulson, Treasury Secretary Henry Paulson stressed that the bailout was to prevent a massive, potentially worldwide financial melt-down, not to bail out investors who had made a poor bet on the companies, or who believed that the fact FNM and FRE are government backed meant their investments were without risk.

The question is now whether this move is enough to turn the markets around, speed stocks to recovery and move our economy toward productive growth. Though stocks surged today, up almost 3% today, there still remains great uncertainty whether this move will actually solve the problems we face today.

What do I think? Honestly, while I think the move is a needed one to prevent a much larger problem, I do not believe that our economy will be magically cured over night by the move. Home prices are continuing to fall, and until they trough and begin to recover, defaults will rise, write-downs will mount and the overall economy will be shaky. I do, however, think that this could be the bottom for some stocks, if not the market in general. Last time the government made a large, unprecedented move to keep the markets afloat, after Bear Sterns, we enjoyed a few months of higher levels of trading before the bears came again. I think that we will definitely see stocks trading up, but they may actually stay high this time. The dollar is recovering, but it is still low enough to keep exports high, and commodities, especially oil, are trading down due to crack downs on speculation in these markets.

Overall, I think that this will be very interesting next few months. Hopefully stocks will recover, banks will start to find a foothold and buying opportunities will present themselves. The main indicator I will be watching is home prices and defaults. If you think you see a bottom in prices or a top in defaults, I'd say that's the time to jump in. I think home prices will continue to drop, however, though not as much as predicted in my last article because this move by the government will stabilize the housing market. I'm gonna watch closely and wait for this to happen.

Monday, August 11, 2008

Visa's Growing Pains

I touted Visa at its IPO because it had such huge interest and momentum, and because it seemed a no brainer at the time. I wasn't alone, as millions made a quick 30% buying in around $60 a share the days after the IPO pricing, and the lucky few who got in at IPO could have easily doubled their money. However, the fun is over. If this stock was the baby that could do no wrong, its now the annoying toddler who can't walk and can barely string together sentences consisting of a few pronouns. Visa has been shunned by investors as profits have been taken and interest has waned. The high of 89.84 hit in early May hasn't been seen since, as the stock is currently trading at 74.79 a decline of 16.75%. The stock has traded sideways/slightly downwards since the incredible run up. Right now the stock faces close resistance around 75 and close support around 70. Personally I hate this because while I have positions in at $60, I'm also in at an average around $76. I would be swing trading the crap out of this stock right now if I had the extra bank, but right now all my extra is tied in with Visa. Anyway, the point of this article isn't to bitch about my frustrations, it's to try to provide some optimism to others long on V.

Why am I optimistic? And it's not just that I have money tied into Visa's stock. It's that and some other things.

1. Visa does not issue lines of credit, so it is not affected by credit market deteriorating as banks are. I think that one of the huge issues weighing on Visa's share price is the continued trouble within the financial sector as a whole. It is obvious that Visa is technically a financial stock, however it doesn't make its money the way a bank or other credit lender does. Visa issues the credit card, (and the network needed for the transaction) and then takes a piece of each purchase made with the card. Visa holds no responsibility if those card holders pay their bill; Visa makes money regardless.

2. The impact of the decrease in consumer spending will be dampened for Visa. While it's true less spending means less fees collected by Visa, the fact that the economy is doing poorly and inflation, especially in gas, is rising means people have less available disposable income. While this is leading to the decrease in consumer spending, it also means people have less available physical cash to spend. Paychecks are less, bank accounts are dwindling, and so people must borrow now in order to buy the essentials. Spending with credit cards, as a proportion of all sales, will rise. While macro spending will undoubtedly be a hindrance for Visa, the fact that more spending via credit cards will increase will cancel out much of the pain.

3. Visa is performing. Recently Visa beat analyst earning expectations of .48 by 11 cents. That's over 22% surprise. Shares surged, even breaking the $80 barrier in After Market Trading on July 30th. However, MasterCard's lackluster earnings, due to a one time litigation bill, brought shares back into the rut.

I expect Visa to continue to beat earnings, and at some point investors will become rational again and see that Visa is a winner among a myriad of financial losers. Visa is a solid company that's business model is one of the few that will remain virtually unscathed by the current credit market and macro economic conditions. If your long on Visa, stay strong. This stock is a winner and will eventually get the treatment by investors it deserves.

Why am I optimistic? And it's not just that I have money tied into Visa's stock. It's that and some other things.

1. Visa does not issue lines of credit, so it is not affected by credit market deteriorating as banks are. I think that one of the huge issues weighing on Visa's share price is the continued trouble within the financial sector as a whole. It is obvious that Visa is technically a financial stock, however it doesn't make its money the way a bank or other credit lender does. Visa issues the credit card, (and the network needed for the transaction) and then takes a piece of each purchase made with the card. Visa holds no responsibility if those card holders pay their bill; Visa makes money regardless.

2. The impact of the decrease in consumer spending will be dampened for Visa. While it's true less spending means less fees collected by Visa, the fact that the economy is doing poorly and inflation, especially in gas, is rising means people have less available disposable income. While this is leading to the decrease in consumer spending, it also means people have less available physical cash to spend. Paychecks are less, bank accounts are dwindling, and so people must borrow now in order to buy the essentials. Spending with credit cards, as a proportion of all sales, will rise. While macro spending will undoubtedly be a hindrance for Visa, the fact that more spending via credit cards will increase will cancel out much of the pain.

3. Visa is performing. Recently Visa beat analyst earning expectations of .48 by 11 cents. That's over 22% surprise. Shares surged, even breaking the $80 barrier in After Market Trading on July 30th. However, MasterCard's lackluster earnings, due to a one time litigation bill, brought shares back into the rut.

I expect Visa to continue to beat earnings, and at some point investors will become rational again and see that Visa is a winner among a myriad of financial losers. Visa is a solid company that's business model is one of the few that will remain virtually unscathed by the current credit market and macro economic conditions. If your long on Visa, stay strong. This stock is a winner and will eventually get the treatment by investors it deserves.

Thursday, July 17, 2008

New SEC Governance: Mixed Blessing

The SEC has decided that short selling has gotten out of hand. The practice in which shares are borrowed and sold, hoping to be bought again at a lower price and returned in order to generate profits when a stock is falling, is a common practice among investors who feel a stock is overpriced. Financial stocks have been shorted heavily in the past year, Bear Sterns Cos (BSC) being case in point. When it was rumored to be in trouble, millions of shares were shorted, aiding the downfall of the company.

Today the SEC moved to curb excessive short selling by eliminating 'naked shorting' in which shares aren't actually borrowed. The idea is that as long as the institution could obtain shares it can allow shorting, it doesn't actually have to go through with the process of finding them. Starting Monday the practice will no longer be considered legitimate. Financial stocks which have bear ed the brunt of the short sellers rose hugely today, as investors bet the prices will start to rise once naked shorting is ended. Examples include Lehman Bros (LEH) which has risen over 50% since Tuesday, and Citigroup (C) which rose over 18%. Also seeing some day light are government backed Fannie Mae (FNM) and Freddie Mac (FRE) which are up 12.33% and 17.16% respectively.

This ruling is in a way a double edged sword for financial stocks. In the short term, it provides much needed relief from the battering their stocks were taking from short sellers. Also, it gives confidence to investors that the government will not stand for speculation to get in the way of the macro economy functioning. This can be seen from the recent price jumps. However, in the longer term, it may end up keeping profits down in the future. Many of these companies profit from not only arranging naked shorting, but do it themselves. The elimination of the practice, and continuing regulation by the government could cut into the incomes of these financial stocks in the future.

I am overjoyed that the market actually had a couple successful days among the weeks of crap we have seen, but I do find it interesting that this may come back to haunt the same institutions that are reaping the benefit currently. I'm hoping that the bulls can find their legs again, at least among deserving companies. I think that they may have gotten a little closer these past couple days.

Today the SEC moved to curb excessive short selling by eliminating 'naked shorting' in which shares aren't actually borrowed. The idea is that as long as the institution could obtain shares it can allow shorting, it doesn't actually have to go through with the process of finding them. Starting Monday the practice will no longer be considered legitimate. Financial stocks which have bear ed the brunt of the short sellers rose hugely today, as investors bet the prices will start to rise once naked shorting is ended. Examples include Lehman Bros (LEH) which has risen over 50% since Tuesday, and Citigroup (C) which rose over 18%. Also seeing some day light are government backed Fannie Mae (FNM) and Freddie Mac (FRE) which are up 12.33% and 17.16% respectively.

This ruling is in a way a double edged sword for financial stocks. In the short term, it provides much needed relief from the battering their stocks were taking from short sellers. Also, it gives confidence to investors that the government will not stand for speculation to get in the way of the macro economy functioning. This can be seen from the recent price jumps. However, in the longer term, it may end up keeping profits down in the future. Many of these companies profit from not only arranging naked shorting, but do it themselves. The elimination of the practice, and continuing regulation by the government could cut into the incomes of these financial stocks in the future.

I am overjoyed that the market actually had a couple successful days among the weeks of crap we have seen, but I do find it interesting that this may come back to haunt the same institutions that are reaping the benefit currently. I'm hoping that the bulls can find their legs again, at least among deserving companies. I think that they may have gotten a little closer these past couple days.

Sunday, July 6, 2008

Why I think the Housing Bubble is Barely Burst

So I did a research project/paper this past winter/spring about US homes prices, whether or not prices were a bubble and what was going to happen if indeed the market was inflated. I concluded that yes there was a bubble, it had already started to collapse and it would probably continue for a while because prices seemed to have rose way too rapidly over the past decade.

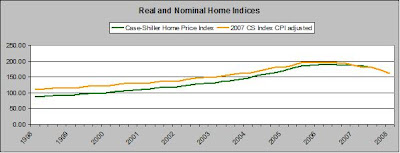

What I didn't realize was how inflated home prices were. A little background info is needed before I start. Dr. Robert Shiller, a professor at Yale and foremost economist when it comes to home prices, wrote a book called Irrational Exuberance in 2000 in which he predicted the tech bubble burst. Then in 2005, he re-released the book with new content that essentially called out the housing bubble burst. He shows in the book through a exhaustive index he created charting home prices that on average, prices rise about .4% a year, when inflation is factored in. From 1940 to 2000, prices rose an average of .7% a year. You get the idea that homes are not great investments from a pure, return-oriented view.

So, how much did homes increase in real value from 1987-1997? None. Actually less than none: -8.46%. The next decade? Home prices increased in real value 82.55% from '88 to their peak in real value in late 2005. Nominal (or not adjusted for inflation) values peaked in 2nd Quarter 2006. Comparing the two decades shows a sharp contrast.

What makes me believe that home prices still have a ways to fall is not simply how inflated prices were, but why they were so inflated. Home prices were so inflated because of increased demand for homes, fueled by a huge increase in credit availability. Basically, when more people can buy homes, demand increases and prices do too. It's not hard to see that right now credit is being restricted and new loans are subject to scrutinization as apposed to securitization. Home prices were a large, juicy bubble, growing ever bigger by lenders, real estate agents and consumers who all believed they could ride the bubble endlessly. They were wrong. All bubbles eventually pop. Whether it be the Stock Market Crash or the tech bubble, when prices are growing only because people expect them to continue to climb, there is a bubble present. Watching home prices tumble and comparing them to technology stocks' plummet in 2000 is easy to do, and probably a reasonable jump to make. While homes have greater intrinsic value than domain names with 25 million in short term debt with no revenue stream did in 2000, they both grew in price because of irrational exuberance, and were brought down by rational investors who figured the bubble out.

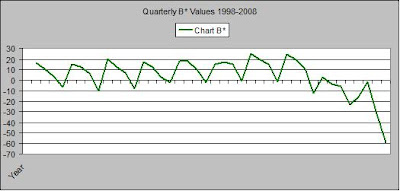

I did some analysis of the data i collected from my paper, updated it, and tried to get an idea of how far prices need to fall in order to be back down to a 'fair' level. What I found shocked me. I'm not going to pretend for a second that I am some sort of math wizzzzard who can predict all markets, but this model did predict prices to fall by a ton, which they have been doing. Basically, I derived a variable, Beta, that is an indicator of how overprices or under priced a asset is. A Beta of 1 means perfectly priced, under 1 ins undervalued and vice versa. Below is the Beta values by quarter over the past decade.

I integrated the curve charting quarterly Beta values and found the displacement from where they should be (equilibrium.) Then I looked at how much they have been displaced so far since the bubble 'burst.' I took A-B=C. C being the amount left to burst. Then I used that number to find out how much prices would fall. The number? 41.209% Shhhhhit.

Do I think home prices will fall 41.209% No. Close to that? Probably not. This number was generated using the assumption of .7% real increase a year being the expected return of a home, and I think that that number is dated. It does show, however, how far prices could fall if long run historical norms are still relevant. I suspect that if prices fall another 20%-25%, buyers will flood the market and prices will begin to return to normal. However, I expect prices to fall at least another 15%-20%, and home prices will probably not return until normal for at least 2 or 3 years.

What does all this mean? It means don't make any investments planning on homes prices rebounding any time soon. Default rates will stay dismal as long as home prices are low, which means more write downs for banks. We're seeing this already, and I think it may continue in a slow and painful way for a while. It doesn't mean I think the stock market will be poor for another 3 years, or even that financial stocks will. But companies that have direct exposure to home prices may be hurting for the short term. Take this with a grain of salt. Do your own research, and let me know what you think. If you would like a more detailed explanation of the model I'm using, or have questions/comments/criticisms, hit me up. (drewo88@hotmail.com)

Friday, July 4, 2008

What To Do Now

While watching the market tank everyday-many days opening high and then crashing after a couple of hours-has me down. As I said before, I thought that the worst was behind us, and I was wrong. Since I started sharing my long term picks on this site (see lower left) The S&P 500 is down more than 5%, but the worst part is that the market had jumped over 7% before losing it all and then some. This makes me sad because I feel like a optimistic dumb-ass. I lost about 15% on holding Citigroup (C) long, and finally closed out a little while ago, feeling that I might as well cut some losses. I also closed out the long position on Vale ADR (RIO), as I felt bears were swamping almost all stocks, and I'd like to preserve some gains.

However, I did add one long position to my portfolio: Wal-Mart (WMT.) As I have talked about before (See My recession article ) I think WMT is a great play when the economy is doing ugly things. While low consumer sentiment, high unemployment and even higher gas prices may seem like big negatives for a retailer, WMT is different. Wal-Mart provides really cheap, yet quality goods, which is good for people who feel the economy is doing poorly and don't have jobs but still need food and toilet paper. Also, WMT has pretty much everything you could need at one location, and so for those who don't feel like driving around on $5 gas it serves as a one stop shop. All of these bode well for WMT. They keep costs low, drive away competition because of it and when people are short on cash, look incredibly attractive when it comes to buying the necessities. They also look good to me as a company that can survive these dire times.

However, I did add one long position to my portfolio: Wal-Mart (WMT.) As I have talked about before (See My recession article ) I think WMT is a great play when the economy is doing ugly things. While low consumer sentiment, high unemployment and even higher gas prices may seem like big negatives for a retailer, WMT is different. Wal-Mart provides really cheap, yet quality goods, which is good for people who feel the economy is doing poorly and don't have jobs but still need food and toilet paper. Also, WMT has pretty much everything you could need at one location, and so for those who don't feel like driving around on $5 gas it serves as a one stop shop. All of these bode well for WMT. They keep costs low, drive away competition because of it and when people are short on cash, look incredibly attractive when it comes to buying the necessities. They also look good to me as a company that can survive these dire times.

Thursday, June 26, 2008

The Market

So a while back, when I first started this blog, I thought that the market had bottomed out. March 10 was the day I thought to be the bottom. Right around this time Bear Sterns had collapsed and been partially saved by the Fed and partially saved by JP Morgan. The S&P 500 Index hit 1273.37, and began to slowly, with great volatility move upwards. However, since the 08 peak in May, the market has lost almost all of its gains. Its down a little more than 10% since May 19th, and currently just above 2008 lows. If the market moves below this, which has been acting as a support, stocks could continue to fall for months.

Because I'm beginning to realize I was premature in calling a bottom (though theoretically March 10 still is the bottom) I think that some of my stock picks should be reassessed. I picked Citigroup back in March, with a price of 20.71 a share. Obviously now is a better time to buy, as you can get shares for 3 bucks cheaper. However, I would hold off on C, wait for any more write downs, analyst downgrades or macroeconomic bad news. Citi might drop even further, which could spell an even better entry point for what I still believe to be a good long term play.

I want to reiterate that most of my picks have done well regardless of the current demise because they are strong companies which were completely undervalued during the last round of market lows. There are many more out there, and even more that overall market sentiment is down so far.

I'm waiting for a sell off in companies like Apple and other solid companies who are not affected directly by sub-prime/credit losses. I missed getting in on this sell off last time (except I did recommend buying AAPL) and I've regretted it. Below I've included a couple of entry points for some stocks I'm watching. These entry points are based on the previous sell off, some technicals and looking at price valuations.

Google Inc. (GOOG)

Buy target: $500

Fwd P/E at this price: 24.85

Apple Inc. (AAPL)

Buy target: $150

Fwd P/E at this price: 28.85

Research in Motion (RIMM)

Buy target: $100

Fwd P/E at this price: 25.77

Wal Mart Stores Inc. (WMT)

Buy target: $55

Fwd P/E at this price: 15.89

Because I'm beginning to realize I was premature in calling a bottom (though theoretically March 10 still is the bottom) I think that some of my stock picks should be reassessed. I picked Citigroup back in March, with a price of 20.71 a share. Obviously now is a better time to buy, as you can get shares for 3 bucks cheaper. However, I would hold off on C, wait for any more write downs, analyst downgrades or macroeconomic bad news. Citi might drop even further, which could spell an even better entry point for what I still believe to be a good long term play.

I want to reiterate that most of my picks have done well regardless of the current demise because they are strong companies which were completely undervalued during the last round of market lows. There are many more out there, and even more that overall market sentiment is down so far.

I'm waiting for a sell off in companies like Apple and other solid companies who are not affected directly by sub-prime/credit losses. I missed getting in on this sell off last time (except I did recommend buying AAPL) and I've regretted it. Below I've included a couple of entry points for some stocks I'm watching. These entry points are based on the previous sell off, some technicals and looking at price valuations.

Google Inc. (GOOG)

Buy target: $500

Fwd P/E at this price: 24.85

Apple Inc. (AAPL)

Buy target: $150

Fwd P/E at this price: 28.85

Research in Motion (RIMM)

Buy target: $100

Fwd P/E at this price: 25.77

Wal Mart Stores Inc. (WMT)

Buy target: $55

Fwd P/E at this price: 15.89

Thursday, June 19, 2008

Fly or Flop: Electro-Optical Science (MELA)

Electro-Optical Science (NASDAQ:MELA) is a small cap ($122.14M) company that is pretty one dimensional. MELA is a firm that's goal is to produce a non-invasive way to diagnose melanoma. It has been public since late October of 2005, and traded side ways since. Currently MELA is trading right under $8 a share (7.93 close today) down from high close of $9.30 May 30th.

However, the price right now is really irrelevant. MELA is going to release results from the trials they are running with their flagship product, MelaFind, this year. If successful, MelaFind would essentially change the way melanoma is diagnosed. Currently, biopsies are performed in order to determine if a mole has cancer. However, this procedure leaves scarring and is expensive. MelaFind would be able to detect cancer without these side effects.

I'm no expert on cancer, medicine, or even health care companies. (Or really any companies for that matter.) But I can see that this company's product has the potential to be in huge demand. The question is whether or not the product will be approved. And that's a big question. If MelaFind doesn't pan out, the company is essentially worthless, at least until they made major changes. The stock would plummet. However, if it does work, there is no doubt it would be incredibly lucrative for any stock holders. A buy out would be a big possibility, which could double or triple current price. Also, the company has enough cash to potentially market MelaFind themselves.

Analysts appear to be optimistic about the company. It has an average rating of 1.7 (1 being strong buy, 5 being strong sell) according to Yahoo Finance. Recently the company briefed investors on the PreMarket Approval (PMA) process at the Needham Biotechnology and Medical Technology Conference in New York. The President & CEO Dr. Joseph Gulfo mentioned he is looking forward to a "busy" end of the year.

I think that the prospects of this company are pretty good. There is a sizable chance that the product could fail, but the studies already performed have yielded great results. Right now melanoma detection is a crude science, which basically involves carving up the patient. Melafind is poised to change all of this. Also, if it succeeds, MELA will see huge growth. There are no other products to suck away profits, this company has put all its eggs in the MelaFind basket.

However, the price right now is really irrelevant. MELA is going to release results from the trials they are running with their flagship product, MelaFind, this year. If successful, MelaFind would essentially change the way melanoma is diagnosed. Currently, biopsies are performed in order to determine if a mole has cancer. However, this procedure leaves scarring and is expensive. MelaFind would be able to detect cancer without these side effects.

I'm no expert on cancer, medicine, or even health care companies. (Or really any companies for that matter.) But I can see that this company's product has the potential to be in huge demand. The question is whether or not the product will be approved. And that's a big question. If MelaFind doesn't pan out, the company is essentially worthless, at least until they made major changes. The stock would plummet. However, if it does work, there is no doubt it would be incredibly lucrative for any stock holders. A buy out would be a big possibility, which could double or triple current price. Also, the company has enough cash to potentially market MelaFind themselves.

Analysts appear to be optimistic about the company. It has an average rating of 1.7 (1 being strong buy, 5 being strong sell) according to Yahoo Finance. Recently the company briefed investors on the PreMarket Approval (PMA) process at the Needham Biotechnology and Medical Technology Conference in New York. The President & CEO Dr. Joseph Gulfo mentioned he is looking forward to a "busy" end of the year.

I think that the prospects of this company are pretty good. There is a sizable chance that the product could fail, but the studies already performed have yielded great results. Right now melanoma detection is a crude science, which basically involves carving up the patient. Melafind is poised to change all of this. Also, if it succeeds, MELA will see huge growth. There are no other products to suck away profits, this company has put all its eggs in the MelaFind basket.

Check out the Electro-Optical Science website for more.

You can see the Needham Biotech presentation on the Investor Relations section.

Thursday, June 12, 2008

Don't be a Greedy Dumb Ass Like Me

So I'm writing today to talk about screwing up. I've been riding high recently, mostly on my investment in Visa (V.) This made me cocky, and also stupid. I decided to try some swing trades, pretty much going off of nothing. Let's just say I learned a lot.

Here is the situation:

Kodiak Oil and Gas Corp. (AMEX: KOG) is a pretty volitle little stock. Its way up this year, but I looked at it after it hit $4.00 a share, a recent high. From there I  figured it would drop, which it did from the beginning. However, it kept dropping. I was looking for an entry point, and I bought soon after the mega drop (see chart 1) at $3.60 and $3.72. I sold some shares right before close at just about $3.80.

figured it would drop, which it did from the beginning. However, it kept dropping. I was looking for an entry point, and I bought soon after the mega drop (see chart 1) at $3.60 and $3.72. I sold some shares right before close at just about $3.80.

figured it would drop, which it did from the beginning. However, it kept dropping. I was looking for an entry point, and I bought soon after the mega drop (see chart 1) at $3.60 and $3.72. I sold some shares right before close at just about $3.80.

figured it would drop, which it did from the beginning. However, it kept dropping. I was looking for an entry point, and I bought soon after the mega drop (see chart 1) at $3.60 and $3.72. I sold some shares right before close at just about $3.80.Pretty sweet right? Nice 5.6% gain in under 2 hours. But the problem was I got greedy. I kept a majority of shares waiting for $4.00 again. I watched shares the next day open at $3.60 settting off a my stop sell order at $3.70. Ouch.

It doesn't end there. I figured I had avoided much of the worst, and so I kept watching the stock. On Tuesday I watched shares continue their demise, and waited for a entry point. After seeing the trough at around $3.40 for about 30 minutes (see below chart), I missed the boat and couldn't get a price below $3.49. I wasn't worried however, because I was counting on a return to $3.65-3.70 and making up my losses from the day b efore. However, shares didn't rise above $3.55, and I ended up keeping shares overnight (BAD IDEA.) I missed selling at $3.60 the next day, getting really greedy, and came back a little later to see prices were wayyyy down. Today I'm looking at KOG pricing between $3.25 and $3.40. Pretty sucky.

efore. However, shares didn't rise above $3.55, and I ended up keeping shares overnight (BAD IDEA.) I missed selling at $3.60 the next day, getting really greedy, and came back a little later to see prices were wayyyy down. Today I'm looking at KOG pricing between $3.25 and $3.40. Pretty sucky.

efore. However, shares didn't rise above $3.55, and I ended up keeping shares overnight (BAD IDEA.) I missed selling at $3.60 the next day, getting really greedy, and came back a little later to see prices were wayyyy down. Today I'm looking at KOG pricing between $3.25 and $3.40. Pretty sucky.

efore. However, shares didn't rise above $3.55, and I ended up keeping shares overnight (BAD IDEA.) I missed selling at $3.60 the next day, getting really greedy, and came back a little later to see prices were wayyyy down. Today I'm looking at KOG pricing between $3.25 and $3.40. Pretty sucky. This is the epitome of crappy, stupid, pathetic day trading at it's worst. I gave up taking 5.6% gains in favor of chasing more. Then I tried to win my losses back by trading the same stock in the same way, and not taking gains when I had them. DON'T LET THIS HAPPEN TO YOU!!!!!

My strategy for these trades was sound. I looked for waining negative volume, bought at a low price and watched the price grow, however, I got greedy and couldn't sell for a small gain. Now I'm faced with stupid losses, and have to either hold onto a stock like KOG, or else sell for a sizable loss. Lesson: Be smart with swing/day trading. Remember, if you make just 1% a day after fees and commissions, your making over 200% a year.

Thursday, May 22, 2008

WiMax Creates Huge Investment Opportunities

Wireless Internet is pretty sweet. But its not perfect, in fact its far from it. The range on most wireless is in the hundreds of feet, providing little maneuverability and restricting use. While you can easily get service anywhere within your home, getting service anywhere around town is nearly impossible, unless your lucky and your town has wireless. WiMax is a joint venture between some tech giants, Google (GOOG), Time Warner (TWX), Intel (INTC), Sprint Nextel (S) and also the lesser known Clearwire (CLWR). The basic idea is creating a wireless network that has the range of a cell phone (several miles) with greater bandwidth than current wireless networks. While there have been a few attempts at similar projects before, this one may be different due to the huge players involved. While it poses some upside for these big companies, it may do the most for the smaller Clearwire. Clearwire is a builder and manager of broadband networks. It stands to profit hugely if WiMax succeeds, as it would probably be acquired by Sprint, or another of the larger backers.

WiMax may become the next step in communication, and the seriousness of this venture can be seen by the involvement of Google, Time Warner and Intel. This deal, if successful, will change the way that we communicate, and also will change the mobile phone market, as demand for this product will sky rocket. Getting a little exposure, or at least keeping tabs on this story, is a good bet.

WiMax may become the next step in communication, and the seriousness of this venture can be seen by the involvement of Google, Time Warner and Intel. This deal, if successful, will change the way that we communicate, and also will change the mobile phone market, as demand for this product will sky rocket. Getting a little exposure, or at least keeping tabs on this story, is a good bet.

Sunday, May 4, 2008

Why Buffet is loving the Credit Crunch

Warren Buffet is many things. Richest man in the world (worth over $60 billion,) Business man (CEO and founder of Berkshire Hathaway,) and philanthropist (donated billions to Gates Foundation.) However, he is also the most celebrated and well known investor ever. His fortune has been made by buying up quality companies at discount prices, and his simple investment strategies trump the confusing and complicated systems that many investors try to use.

So Why is Buffet loving the current economic situation? Because of the one word that could be used to describe Buffets strategy. Value.

The current trouble amid financial sector, and spread to overall macro economy, has presented an opportunity to acquire companies on the cheap. Already, Buffet has showed interest in the Bond Insurance business, announcing willingness to bail out the depressed giants of the industry. Buffet didn't stop there. When he saw that most of the firms within the sector were at their knees due to the sub prime fiasco, he opened his own Bond Insurer, under the Berkshire name. It already has received triple-A ratings from Moody's, and are already drawing many customers from the former industry leaders, MBIA (NYSE:MBIA) and Ambak (NYSE:ABK).

Outside of the financial sector, Buffet has seen value at a discount in Wrigley, the gum maker, as Mars, a Berkshire company purchased Wrigley for $23 billion. Buffet also has announced plans to invest more heavily in Europe as well as South Korea.

The current situation does not only present options for Warren Buffet, it presents opportunities for you as well. Value is something that can be found by everyday investors, and there is a lot of value out there right now. However, there are also many busts out there. Doing homework and evaluating the economics within a potential investment are crucial before making a buy.

So Why is Buffet loving the current economic situation? Because of the one word that could be used to describe Buffets strategy. Value.

The current trouble amid financial sector, and spread to overall macro economy, has presented an opportunity to acquire companies on the cheap. Already, Buffet has showed interest in the Bond Insurance business, announcing willingness to bail out the depressed giants of the industry. Buffet didn't stop there. When he saw that most of the firms within the sector were at their knees due to the sub prime fiasco, he opened his own Bond Insurer, under the Berkshire name. It already has received triple-A ratings from Moody's, and are already drawing many customers from the former industry leaders, MBIA (NYSE:MBIA) and Ambak (NYSE:ABK).

Outside of the financial sector, Buffet has seen value at a discount in Wrigley, the gum maker, as Mars, a Berkshire company purchased Wrigley for $23 billion. Buffet also has announced plans to invest more heavily in Europe as well as South Korea.

The current situation does not only present options for Warren Buffet, it presents opportunities for you as well. Value is something that can be found by everyday investors, and there is a lot of value out there right now. However, there are also many busts out there. Doing homework and evaluating the economics within a potential investment are crucial before making a buy.

Friday, April 18, 2008

Fabulous Friday

Today the market is exploding. As of right now, the S&P 500 is up 1.99%, up on news that Google's ad-click business seems to be unaffected by macroeconomic downturns, Citigroup's earnings report which topped analysts expectations and general positive investor sentiment. Earnings released this week by large banks indicate that losses have no been as large has predicted, and investors are moving back into the market. Not only are financial stocks up, but technology is showing strong growth on the Google news, and also as investors move back into the market, tech stocks will see a lot of this action. Citigroup is up 7.24% and Google is up 21.09% today. The aggregate tech sector is up 2.62%, Financials are up 2.02%, and Capital Goods are seeing the best day by sector, up 2.68%.

Today marks a big day for the market. The market will close today for the weekend. This will mean the market has closed up for the week, showing that investors feel comfortable will sustainable price increases, bucking the trend of volatile and up-down markets. While there may be a sell-off early next week, I see this as a buying opportunity, as I expect the markets to continue to grow from here on.

Today marks a big day for the market. The market will close today for the weekend. This will mean the market has closed up for the week, showing that investors feel comfortable will sustainable price increases, bucking the trend of volatile and up-down markets. While there may be a sell-off early next week, I see this as a buying opportunity, as I expect the markets to continue to grow from here on.

Tuesday, April 15, 2008

Earnings Week

The current week is a big one for the Street, as many of the biggest companies release earnings. It's potentially make or break for the health of the market, as stocks have remained stagnant since the S&P jumped 47.48 points April 1st. Since then, the market has lost its gains, but seems to be waiting for news that will either propel prices back up, or slam them back down. This weeks earning announcements seem like the catalyst investors have been waiting for.

The disappointing earnings reported by bellwether General Electric (NYSE:GE) saw stocks plunge on Friday, a sign that investors are keenly watching earnings as a sign of how companies aer performing. Earnings are expected to increase 15.7% in 2008, which is a daunting figure. Earnings in 2007 were supposed to increase 14.5%, and are now thought of to have rose only 2.6%. If companies can't perform as expected, we could be looking at more declines and a continuation of this bear market. However, if earnings are reasonable, investors may be confident enough again to return to stocks, many of which are trading at a huge discount.

While there are many companies reporting this week, there are a few that I feel are the most important company reporting tomorrow, Wednesday April 16th:

The disappointing earnings reported by bellwether General Electric (NYSE:GE) saw stocks plunge on Friday, a sign that investors are keenly watching earnings as a sign of how companies aer performing. Earnings are expected to increase 15.7% in 2008, which is a daunting figure. Earnings in 2007 were supposed to increase 14.5%, and are now thought of to have rose only 2.6%. If companies can't perform as expected, we could be looking at more declines and a continuation of this bear market. However, if earnings are reasonable, investors may be confident enough again to return to stocks, many of which are trading at a huge discount.

While there are many companies reporting this week, there are a few that I feel are the most important company reporting tomorrow, Wednesday April 16th:

- Wells Fargo & Co. (NYSE:WFC) reports Wednesday. The financial institution has been hit by subprime exposure and the overall liquidity crisis. They are the 8th largest member of the Money Center Bank sector, with a Market Cap of 90.9 Billion. Earnings are forecast for $.57 for the quarter, and $2.42 for the current year. 4Q 2007 earnings were $.41, and last years earnings were $2.38. Intraday price as of 2 pm Tuesday April 15 was 27.68, up 1.73% from previous close.

- The Coca-Cola Co. (KYSE:KO) reports Wednesday as well. The beverage producer has seen explosive growth from over seas and a weak dollar has helped exports. Expansion in developing markets, such as China, should have offset the weak economy in the US. KO is doing much better than most stocks, its down .81% in 2008. However, this earnings report will show if the economic contraction at home is cutting into KO's profitability more than expected. Expectations from analysts are $.62 per share.

- JP Morgan Chase Co (NYSE:JPM) reports on Wednesday. The financial giant that recently purchased Bear Sterns Cos at a huge discount has seen its share price sky rocket since the acquisition. However, the buy out could have hurt profits this quarter. JPM is expected to post earnings of $.64 earnings per share. Meeting the expectations could show that JPM did not sacrifice large amounts of money to make the purchase, and position it as the premiere financial company. A miss could be seen by investors as a sign of weakness, though investors might forgive a miss because of the recent Bear Sterns buy out.

Monday, April 7, 2008

Tech Sector Upside

The Technology sector has been battered over the past few months as stocks tumbled and the economic situation deteriorated. The sector is down -12.4% this year. However, before the recent catastrophe, the tech sector was growing quite nicely. In fact, it was up 108.5% since October of 2002. This is second only to the Energy sector. Tech stocks grew an average of 14.63% per year over the past seven odd years. Unlike real estate and some financial stocks, this was not due to irrational exuberance or bubble atmosphere, but on new innovation, higher demand and better productivity. Look at the iPod, the progression of computers, the speed of Internet, Google and HiDef televisions.

So whats changed? Why are tech stocks doing so terribly? Well, I'm not positive. But a lot of it has to do with investor sentiment. Investors leaving the stock market and pulling out of very popular stocks. Many of these are technology sector firms, like Google. This has proved deadly for stocks within the technology sector. Also, there is the real fact that people buy less tech goods during a recession, (do you buy the iPod or the groceries?) However, higher demand from overseas will counteract this to some degree. This can be attributed to the ever growing middle class of India and China, and the weak dollar making our products seem cheaper. Even if some of the price decreases are warranted by decrease demand for technology, I think these stocks still present a unique value buy.

The graph above shows the S&P Technology Sector Index. It shows the massive losses that the sector has experienced over the past year. The sector is down -12.7% in 2008, compared with -6.53% for the S&P at large. For contrast, the Financial Sector is down -8.92% in 2008. This means the tech sector is performing worse than the financial stocks that are right in the middle of the meltdown.

The Tech sector represents a huge value opportunity right now simply because the stocks have been beaten so low. Like financial stocks, these companies are trading at fractions of what they were a year ago. However, unlike financials, they have no real flaws behind them. These companies are not going anywhere, and if your willing to wait for a little bit, they will yield HUGE returns in the coming months.

Top Tech Stocks

Google Inc. (NASDAQ:GOOG)

-Market Cap: 146.60 Billion

-current year forward (CYF) P/E: 23.97

-CYF PEG: .9374

-52 wk HIGH/LOW/CHANGE: 747.24/412.11/-.78%

-YTD HIGH/LOW/CHANGE: 691.48/412.11/-32.35%

Apple Inc. (NASDAQ: AAPL)

-Market Cap: 143.33 Billion

-CYF P/E: 29.68

-CYF PEG: .957

-52 wk HIGH/LOW/CHANGE: 202.96/80.60/61.43%

-YTD HIGH/LOW/CHANGE: 198.08/119.46/-22.84$

Microsoft Corp. (NASDAQ: MSFT)

-Market Cap: 267.58 Billion

-CYF P/E: 15.37

-CYF PEG: .603

-52 wk HIGH/LOW/CHANGE: 37.50/26.87/.7%

-YTD HIGH/LOW/CHANGE: 35.60/26.87/-19.24%

Cisco Systems Inc. (NASDAQ: CSCO)

-Market Cap: 142.81 Billion

-CYF P/E: 15.56

-CYF PEG: 1.044

-52 wk HIGH/LOW/CHANGE: 34.24/21.77/-1.12%

-YTD HIGH/LOW/CHANGE: 27.07/21.77/-11.49%

So whats changed? Why are tech stocks doing so terribly? Well, I'm not positive. But a lot of it has to do with investor sentiment. Investors leaving the stock market and pulling out of very popular stocks. Many of these are technology sector firms, like Google. This has proved deadly for stocks within the technology sector. Also, there is the real fact that people buy less tech goods during a recession, (do you buy the iPod or the groceries?) However, higher demand from overseas will counteract this to some degree. This can be attributed to the ever growing middle class of India and China, and the weak dollar making our products seem cheaper. Even if some of the price decreases are warranted by decrease demand for technology, I think these stocks still present a unique value buy.

The graph above shows the S&P Technology Sector Index. It shows the massive losses that the sector has experienced over the past year. The sector is down -12.7% in 2008, compared with -6.53% for the S&P at large. For contrast, the Financial Sector is down -8.92% in 2008. This means the tech sector is performing worse than the financial stocks that are right in the middle of the meltdown.

The Tech sector represents a huge value opportunity right now simply because the stocks have been beaten so low. Like financial stocks, these companies are trading at fractions of what they were a year ago. However, unlike financials, they have no real flaws behind them. These companies are not going anywhere, and if your willing to wait for a little bit, they will yield HUGE returns in the coming months.

Top Tech Stocks

Google Inc. (NASDAQ:GOOG)

-Market Cap: 146.60 Billion

-current year forward (CYF) P/E: 23.97

-CYF PEG: .9374

-52 wk HIGH/LOW/CHANGE: 747.24/412.11/-.78%

-YTD HIGH/LOW/CHANGE: 691.48/412.11/-32.35%

Apple Inc. (NASDAQ: AAPL)

-Market Cap: 143.33 Billion

-CYF P/E: 29.68

-CYF PEG: .957

-52 wk HIGH/LOW/CHANGE: 202.96/80.60/61.43%

-YTD HIGH/LOW/CHANGE: 198.08/119.46/-22.84$

Microsoft Corp. (NASDAQ: MSFT)

-Market Cap: 267.58 Billion

-CYF P/E: 15.37

-CYF PEG: .603

-52 wk HIGH/LOW/CHANGE: 37.50/26.87/.7%

-YTD HIGH/LOW/CHANGE: 35.60/26.87/-19.24%

Cisco Systems Inc. (NASDAQ: CSCO)

-Market Cap: 142.81 Billion

-CYF P/E: 15.56

-CYF PEG: 1.044

-52 wk HIGH/LOW/CHANGE: 34.24/21.77/-1.12%

-YTD HIGH/LOW/CHANGE: 27.07/21.77/-11.49%

Tuesday, April 1, 2008

Tommorow Big Day for Stocks

Today the market surrrrged. The Dow Jones (DJIA) was up 391.47 points or 3.19% to 12,654.36. The NASDAQ was up 83.65 (3.67%) to 2,362.75, and the S&P 500 was up 47.48 points, 3.59% to 1370.18. Woah. Lots of numbers. Better yet, lots of green numbers. Let me summarize: the markets did work today.

However, if we're ever going to get out of the current slump, which I think we should and will do, the market is going to have to string together consecutive days of good performance. The market looks like it may be at a bottom, but if it just goes back down, were still stuck in our rut. Look at the S&P graph from Google Finance (.INX) to see what I mean.

While I'm no technician (some one who uses graphs and charts to predict the market) I do believe that using technicals can help predict how markets will perform. Looking at this chart shows me that over the past 3 months, in which the market lost 6.69%, there have been distinct support and resistance values for the S&P. You can see the 4 peaks, labelled ABCD, and the downward resistance line they create. You can also see the support line, created by the troughs EFG. Today broke this resistance. While this isn't enough to make market calls, it does show investor sentiment rose a notable amount, as prices broke trends that were keeping them in a downward spiral. Also, news from the Treasury, the extension of Fed's auction window to investment institutions, stimulus package on the way and rallying international markets make me hopeful.

The patterns here are very similar to those of the NASDAQ and the DJIA . (Check out Google Finance for their graphs.) Another thing I find promising about the charts is that one, the S&P was following a distinct trend before 2008 as well. And two, the last time the S&P broke trend, it broke support, and the market began a larger downward trend. (See above graph, the trend lines should be pretty apparent.) Now that it has broken trend again, and this time by breaking resistance, I'm hopeful we'll see an upward trend.

I'm looking at tomorrow as a sort of Grounds-Hog Day. If the market comes out, sees its shadow and dives 2%, we may be back in the rut and today was a fluke. But if we can keep this growth, and add new growth over the coming days without any unexpected bad news, I think we may have weathered the storm. Let's hope for the best.

However, if we're ever going to get out of the current slump, which I think we should and will do, the market is going to have to string together consecutive days of good performance. The market looks like it may be at a bottom, but if it just goes back down, were still stuck in our rut. Look at the S&P graph from Google Finance (.INX) to see what I mean.

While I'm no technician (some one who uses graphs and charts to predict the market) I do believe that using technicals can help predict how markets will perform. Looking at this chart shows me that over the past 3 months, in which the market lost 6.69%, there have been distinct support and resistance values for the S&P. You can see the 4 peaks, labelled ABCD, and the downward resistance line they create. You can also see the support line, created by the troughs EFG. Today broke this resistance. While this isn't enough to make market calls, it does show investor sentiment rose a notable amount, as prices broke trends that were keeping them in a downward spiral. Also, news from the Treasury, the extension of Fed's auction window to investment institutions, stimulus package on the way and rallying international markets make me hopeful.

The patterns here are very similar to those of the NASDAQ and the DJIA . (Check out Google Finance for their graphs.) Another thing I find promising about the charts is that one, the S&P was following a distinct trend before 2008 as well. And two, the last time the S&P broke trend, it broke support, and the market began a larger downward trend. (See above graph, the trend lines should be pretty apparent.) Now that it has broken trend again, and this time by breaking resistance, I'm hopeful we'll see an upward trend.

I'm looking at tomorrow as a sort of Grounds-Hog Day. If the market comes out, sees its shadow and dives 2%, we may be back in the rut and today was a fluke. But if we can keep this growth, and add new growth over the coming days without any unexpected bad news, I think we may have weathered the storm. Let's hope for the best.

Saturday, March 29, 2008

US Companies That Won't Be Hurt By a Recession

There's a lot of talk about a recession. I think we are probably in one, and to be honest, it doesn't really matter if we technically are, because our economy is suffering for sure. This spells trouble for most American businesses, because US consumers will spend less in general as they attempt to weather the economic troubles we face. The media won't help this either, because all the reports about how dismal our economic outlook is only keeps people's money closer to them, and US businesses will feel the hurt.

However, there are some US corporations which won't be hurt by a poor economic situation at home. These companies are insulated from domestic troubles by a variety of reasons. Some face huge demand from overseas Some see increase demand from citizens during rough economic times. Whatever the reason, finding a company like this and investing in it as a hedge against further economic downturns is a good way to grow your money in a time when most stocks are losing ground. Here are a few stocks I feel will not feel the recession, or may actually profit from it:

Wal-Mart (NYSE:WMT)

Wal-Mart (WMT), as we all know, is a huge chain of retail stores that sells everything from groceries to clothing. Known for cheap prices that run competitors out of business, WMT is all about price and not about quality. During rosy economic conditions, Wal-Mart sees large demand for their goods. In a recession, Wal-Mart sees HUGE demand. When consumer confidence is low and people are scared about spending money, they will search out the cheapest prices they can, and they will be willing to sacrifice name brands to do it. For necessities like clothing and food, WMT meets the demands of consumers concerned about cost. This is why Wal-Mart saw same store sales rise 3% in February, and why Analysts project WMT will grow by 12.5% next quarter. WMT will see continued growth throughout 2008, but it will probably peak in about 3-4 months, as the economic slowdown will probably begin to lessen at that point. WMT is up 8.79% from a year ago, and up 9.66% so far this year.

Caterpillar (NYSE:CAT)

Caterpillar (CAT), is the number one company when it comes to industrial, commercial and agricultural machinery and engines. CAT has the largest market share of this sector, with a $48.1 Billion market share. Last year they took in 47% of revenue from overseas, and with urbanization in China and India overseas foreign should see steady growth. This is a huge strength of CAT, it seems to be able to maneuver difficult situations here in the US because it has such a strong presence in other places.

Also, CAT provides products that few, if anyone, else can produce. Take for example the 777F, an enormous truck used in mining that can carry over 100 tons at a speed of 40 mph. No one else in the world can provide these kinds of equipment, and that's why you'd have to wait till 2012 for these bad boys if you bought today, and pay millions of dollars for it.

CAT provides little downside for investors, as it can benefit from basically any situation. Disasters provide the need for earth moving vehicles, economic growth of third world countries requires heavy machinery, and more growth here in the US also spells more demand for CAT's product. While the downside pay be low, CAT is a mature company and has less room for rapid growth than other companies. I see CAT as a low-risk play to balance a portfolio looking for a long term and slow growth winner. CAT is up 15.27% from a year ago, and up 6.24% in 2008.

McDonald's Corp. (NYSE:MCD)

The true king of fast food, McDonald's Corp. (MCD) represents today's society. Get something that's quick, pleasing, and most importantly fast. Do that, and then sell the rights to do that to other people who will do most of the dirty work themselves. Love them or hate them, MCD has it figured out. They run more than 31,000 restaurants, employ over 1.5 million people, and operate in over 100 countries. Not only that, but they do it for less than anyone. These last two reasons are why they survive a recession in the US. Because they have such a huge global market, the slowing the US doesn't kill them. Unlike an energy company that only sells the US citizens, MCD sells in most countries, and they are experiencing rapid global expansion. Secondly, the "dollar menu" looks pretty good during a period of economic decline. The inexpensive food they offer sees large demand when people have less money to spend. MCD is expected by analysts to grow 9.56% annually the next 5 years, and 10.7% this year. They are trading at a forward P/E of 17.34, with a forward PEG of 1.62. While it isn't the best value, MCD offers a steady investment when economic times are bad. This February they reported a 12% gain in same store sales. They are up 23.15% from a year ago, however they are down 5.82% Year To Date.

However, there are some US corporations which won't be hurt by a poor economic situation at home. These companies are insulated from domestic troubles by a variety of reasons. Some face huge demand from overseas Some see increase demand from citizens during rough economic times. Whatever the reason, finding a company like this and investing in it as a hedge against further economic downturns is a good way to grow your money in a time when most stocks are losing ground. Here are a few stocks I feel will not feel the recession, or may actually profit from it:

Wal-Mart (NYSE:WMT)

Wal-Mart (WMT), as we all know, is a huge chain of retail stores that sells everything from groceries to clothing. Known for cheap prices that run competitors out of business, WMT is all about price and not about quality. During rosy economic conditions, Wal-Mart sees large demand for their goods. In a recession, Wal-Mart sees HUGE demand. When consumer confidence is low and people are scared about spending money, they will search out the cheapest prices they can, and they will be willing to sacrifice name brands to do it. For necessities like clothing and food, WMT meets the demands of consumers concerned about cost. This is why Wal-Mart saw same store sales rise 3% in February, and why Analysts project WMT will grow by 12.5% next quarter. WMT will see continued growth throughout 2008, but it will probably peak in about 3-4 months, as the economic slowdown will probably begin to lessen at that point. WMT is up 8.79% from a year ago, and up 9.66% so far this year.

Caterpillar (NYSE:CAT)

Caterpillar (CAT), is the number one company when it comes to industrial, commercial and agricultural machinery and engines. CAT has the largest market share of this sector, with a $48.1 Billion market share. Last year they took in 47% of revenue from overseas, and with urbanization in China and India overseas foreign should see steady growth. This is a huge strength of CAT, it seems to be able to maneuver difficult situations here in the US because it has such a strong presence in other places.

Also, CAT provides products that few, if anyone, else can produce. Take for example the 777F, an enormous truck used in mining that can carry over 100 tons at a speed of 40 mph. No one else in the world can provide these kinds of equipment, and that's why you'd have to wait till 2012 for these bad boys if you bought today, and pay millions of dollars for it.

CAT provides little downside for investors, as it can benefit from basically any situation. Disasters provide the need for earth moving vehicles, economic growth of third world countries requires heavy machinery, and more growth here in the US also spells more demand for CAT's product. While the downside pay be low, CAT is a mature company and has less room for rapid growth than other companies. I see CAT as a low-risk play to balance a portfolio looking for a long term and slow growth winner. CAT is up 15.27% from a year ago, and up 6.24% in 2008.

McDonald's Corp. (NYSE:MCD)

The true king of fast food, McDonald's Corp. (MCD) represents today's society. Get something that's quick, pleasing, and most importantly fast. Do that, and then sell the rights to do that to other people who will do most of the dirty work themselves. Love them or hate them, MCD has it figured out. They run more than 31,000 restaurants, employ over 1.5 million people, and operate in over 100 countries. Not only that, but they do it for less than anyone. These last two reasons are why they survive a recession in the US. Because they have such a huge global market, the slowing the US doesn't kill them. Unlike an energy company that only sells the US citizens, MCD sells in most countries, and they are experiencing rapid global expansion. Secondly, the "dollar menu" looks pretty good during a period of economic decline. The inexpensive food they offer sees large demand when people have less money to spend. MCD is expected by analysts to grow 9.56% annually the next 5 years, and 10.7% this year. They are trading at a forward P/E of 17.34, with a forward PEG of 1.62. While it isn't the best value, MCD offers a steady investment when economic times are bad. This February they reported a 12% gain in same store sales. They are up 23.15% from a year ago, however they are down 5.82% Year To Date.

Thursday, March 27, 2008

Salil Sessions

First of all I’d like to say hello to visitors of this blog. My name is Salil, and I’ll be writing posts from time to time. By the way if “Salil Sessions” seems somewhat familiar it’s because it’s an acknowledgement towards Alan Sloan’s “Sloan Sessions”. I’m a fan of “Sloan Sessions” because he explains complicated situations simply and with what he feels are the best courses of action. Although I do not claim to have his expertise, I hope to emulate his style and add a light hearted feel towards the stock market. That being said, my posts are not going to be comedy pieces and I will always address the situation thoroughly.

Breakfast at Tiffany’s

Well, for those who haven’t seen it, Breakfast at Tiffany’s is an 1961 film (originally a novel by Truman Capote) about a call girl named Holly Golightly (Audrey Hepburn) who meets a failing writer/ gigolo Paul Varjak (George Pappard). Holly has dreams about one day becoming an aristocrat, going to the best parties, and well achieving any girls’ dreams. As any predictable romantic comedy unfolds the girl exchanges her diamonds at Tiffany’s and goes for her true love, and, what do you know? The diamond fell into the laps of Tiffany & Co investors after the company produced better than expected results for their 07 4th Quarter.

So what does this mean for non-investors? Analysts we’re eager to see how Tiffany & Co (TIF) would fare because it would show how the luxury market is doing. After several bad months on Wall Street, a heavily loss in the luxury market would be another huge concern. Although it is certain that average consumers have cut back on spending, if upper income consumers have done the same then there would be a very grim outlook on consumption – which is the majority of the economy.

After Tiffany & Co reports were released the stock went up 10% and there was a silver lining in the clouds. Perhaps the most interesting parts of the report are the specifics. Even though sales fell 4% in the U.S, they increased a staggering 21% internationally. Booming economies in the emerging markets has caused increase in sales in places like Brazil and China, and even though America’s decline in the past few months has certainly had a detrimental affect globally, it hasn’t stopped the emerging upper middle class internationally from buying some diamond rings.

Although there is a possibility that the eventual decline of the euro could affect demand of US companies like TIF, one has to understand that these countries have been rising at huge bounds for the past 10 yrs and they have reached a position they are not going to give back in a 6 month period. According to Mr. Belloni from Pictet (a Swiss investment bank), “They [luxury companies] are very cheap” and some are only 12 to 13 times forward earnings with high yields with huge cash deposits and very little debt. So how would someone in America play the luxury game? Actually it’s kind of hard. With the 3 biggest luxury conglomerates –LVMH, PPR, and Richemont – all traded only on international markets shy of Tiffany & Co. and Diageo (DEO) there aren’t very many big players on the streets of the NYSE. Instead, some feel the best move is to bet on the sector. Claymore Advisers and the magazine,the Rob Report recently launched an ETF called Claymore/ Rob Report Global Luxury (ROB) . Their holdings include BMW, Porshe LVMH, Christian Dior and various others). You can also look at the Bloomberg European Luxury Index and the Merrill Lynch Lifestyle Index.

Although there is a possibility that the eventual decline of the euro could affect demand of US companies like TIF, one has to understand that these countries have been rising at huge bounds for the past 10 yrs and they have reached a position they are not going to give back in a 6 month period. According to Mr. Belloni from Pictet (a Swiss investment bank), “They [luxury companies] are very cheap” and some are only 12 to 13 times forward earnings with high yields with huge cash deposits and very little debt. So how would someone in America play the luxury game? Actually it’s kind of hard. With the 3 biggest luxury conglomerates –LVMH, PPR, and Richemont – all traded only on international markets shy of Tiffany & Co. and Diageo (DEO) there aren’t very many big players on the streets of the NYSE. Instead, some feel the best move is to bet on the sector. Claymore Advisers and the magazine,the Rob Report recently launched an ETF called Claymore/ Rob Report Global Luxury (ROB) . Their holdings include BMW, Porshe LVMH, Christian Dior and various others). You can also look at the Bloomberg European Luxury Index and the Merrill Lynch Lifestyle Index.

Looking at the history of the luxury market in the past 6 months, there has definitely been a decline; however, with heavy amounts of cash and a growing international market this industry might just be a diamond in the rough.

If you have any comments or questions, I would love to hear them. Please let me know what you think of my articles so I can tweak them in the future. You can contact me at salilka@gmail.com . I’d like to thank you for checking out the Salil Session.

Monday, March 24, 2008

ECRO Drops

So I wrote about daytrading a while back, and mentioned ECC Capital Corp (ECRO.) I also mentioned them when I talked about dividends, because they paid such a high one last week. I mentioned how easily it was to trade this stock effectively because of its clear and stable supports and resistance values. However, this all ch anged today as ECRO closed at .11, and traded as low as .095. This is huge drop, -31.25%, probably represents the beginning of a new trend. I would guess that today's close price (around .10 or .11) will become either the new resistance or new support (probably the support) and a new pattern will be determined in the coming weeks. I would stay away from the stock until a pattern emerges, because if you guess and guess wrong, you could stand to loose a TON. I'm guessing that the sell off is due to the dividend being paid out Friday, and today was the first day of trading afterwards. However, the actual reason may be just arbitrary selling by investors, or knowledge of something that happened that I don't have. After the new pattern is set, I think the stock will still be a good one to day trade, because it seems to settle into predictable patterns of established supports and resistance.

anged today as ECRO closed at .11, and traded as low as .095. This is huge drop, -31.25%, probably represents the beginning of a new trend. I would guess that today's close price (around .10 or .11) will become either the new resistance or new support (probably the support) and a new pattern will be determined in the coming weeks. I would stay away from the stock until a pattern emerges, because if you guess and guess wrong, you could stand to loose a TON. I'm guessing that the sell off is due to the dividend being paid out Friday, and today was the first day of trading afterwards. However, the actual reason may be just arbitrary selling by investors, or knowledge of something that happened that I don't have. After the new pattern is set, I think the stock will still be a good one to day trade, because it seems to settle into predictable patterns of established supports and resistance.

anged today as ECRO closed at .11, and traded as low as .095. This is huge drop, -31.25%, probably represents the beginning of a new trend. I would guess that today's close price (around .10 or .11) will become either the new resistance or new support (probably the support) and a new pattern will be determined in the coming weeks. I would stay away from the stock until a pattern emerges, because if you guess and guess wrong, you could stand to loose a TON. I'm guessing that the sell off is due to the dividend being paid out Friday, and today was the first day of trading afterwards. However, the actual reason may be just arbitrary selling by investors, or knowledge of something that happened that I don't have. After the new pattern is set, I think the stock will still be a good one to day trade, because it seems to settle into predictable patterns of established supports and resistance.

anged today as ECRO closed at .11, and traded as low as .095. This is huge drop, -31.25%, probably represents the beginning of a new trend. I would guess that today's close price (around .10 or .11) will become either the new resistance or new support (probably the support) and a new pattern will be determined in the coming weeks. I would stay away from the stock until a pattern emerges, because if you guess and guess wrong, you could stand to loose a TON. I'm guessing that the sell off is due to the dividend being paid out Friday, and today was the first day of trading afterwards. However, the actual reason may be just arbitrary selling by investors, or knowledge of something that happened that I don't have. After the new pattern is set, I think the stock will still be a good one to day trade, because it seems to settle into predictable patterns of established supports and resistance.

Sunday, March 23, 2008

Finding a Brokerage

I'm a high school kid too who's just starting to invest, but I don't know what internet stock broker to use, any advice?

This is a question that was emailed to me yesterday. And honestly, I'm probably not the best person to be giving advice, but I have had my fair share of experience with different brokerages, so I'll give it a shot.

Personally, the biggest thing I look for in a brokerage is the commission fee. For small time investors (like me, and probably you) commissions can make the difference between a gain and a loss. When your buying thousands of dollars worth of stock, a $10 commission is noise. However, when your trading $100 dollars worth of stocks, $10 represents a 10% hit right off the bat, and then it will also take a chunk out of the money you end up selling a stock for. I got in a position with E*Trade where I bought $100 worth of a stock but couldn't sell after a 20% jump because i would actually loose money due to the commissions. Taking into account how much the commission is can not only help you choose a broker, but help you choose the amount your going to invest.

Watch for hidden fees as well. Some brokers offer low fees, but only under certain conditions. One place fees arise that has hurt me is when trading penny stocks. Make sure there are not penalties for investing in low price stocks, or buying a large number of shares.